Summary

- Buffett is no longer a bargain hunter, but Benjamin Graham's framework never was about bargain hunting in the first place.

- Charlie Munger seems to have steered Buffett away from cigar butt stocks, towards following Graham's Value Investing principles in their entirety.

- The size of Buffett's portfolio is also his biggest handicap. The rest of us can actually do better percentages by simply following the more automated forms of Value Investing.

Introduction

Benjamin Graham - also known as the Dean of Wall Street and the Father of Value Investing - was a scholar and financial analyst who mentored legendary investors such as Warren Buffett, William J. Ruane, Irving Kahn and Walter J. Schloss.

Warren Buffett once gave a speech at Columbia Business School explaining how Graham's record of creating exceptional investors (such as Buffett himself) is unquestionable, and how Graham's principles are everlasting. The speech is now known as The Superinvestors of Graham-and-Doddsville [PDF].

But many arguments are put forth today that Buffett is no longer a Value Investor and no longer follows Graham's principles.

Let's examine them one by one.

Contention 1: Buffett Is No Longer A Bargain Hunter

While it is true that Buffett is no longer a bargain hunter, Graham's Value Investing never was about bargain hunting in the first place.

Graham's first recommended strategy was to invest in the stocks comprising an Index. This includes expensive "growth" stocks and is clear refutation of the myth that Value Investing is restricted to cheap stocks and cigar-butts.

For more serious investors, Graham recommended three different categories of stocks - Defensive, Enterprising and NCAV - and 17 qualitative and quantitative rules for identifying them. These can be reliably detected by today's data-mining software, and offer a great avenue for accurate automated analysis and profitable investment.

For advanced investors, Graham described various Special Situations or Workouts. These require more than the average level of ability and experience. Such stocks are also not amenable to impartial algorithmic analysis, and require a case-specific approach.

But most Graham analyses today only follow the quantitative part of Graham's recommendations (NCAV, Graham Number etc.) without the supporting qualitative criteria. Some even use serious misinterpretations of Graham's methods. All this has resulted in the common misconception today that Value Investing is just bargain hunting.

Contention 2: Buffett Was Influenced By Charlie Munger

Munger's influence on Buffett has been discussed often, and the argument is often made that Munger is to be credited - instead of Graham - for Buffett's success in investing.

Here's what Buffett himself wrote about Munger's influence on him:

"It took Charlie Munger to break my cigar-butt habits and set the course for building a business that could combine huge size with satisfactory profits."

There are students of Graham who do focus exclusively on NCAV (or cigar-butt) stocks. The late Walter Schloss was one of them, and it appears, so was Buffett. The NCAV strategy is easy to follow, and very profitable.

But bargain hunting becomes harder as the size of one's portfolio increases. Value Investing is also so much more than cigar-butt stocks and bargain hunting, as described earlier.

Buffett gave The Superinvestors of Graham-and-Doddsville speech in 1984; much after he had started working with Munger.

Buffett's concluded the speech, saying:

"Ships will sail around the world but the Flat Earth Society will flourish. There will continue to be wide discrepancies between price and value in the marketplace, and those who read their Graham & Dodd will continue to prosper."

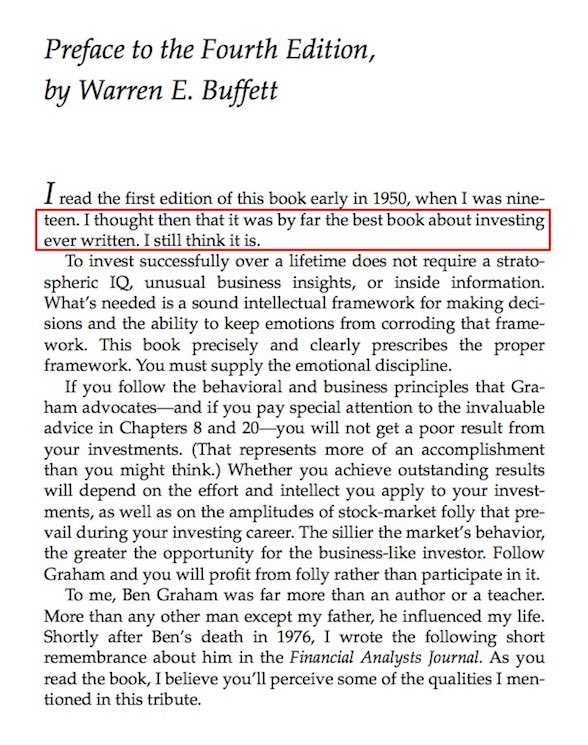

The preface to The Intelligent Investor - in which he calls it by "far the best book about investing ever written" - was written even later, in 1986.

Buffett wrote thus in the preface:

"To invest successfully over a lifetime does not require a stratospheric IQ, unusual business insights, or inside information. What's needed is a sound intellectual framework for making decisions and the ability to keep emotions from corroding that framework. This book precisely and clearly prescribes the proper framework. You must supply the emotional discipline."

Contention 3: Buffett Wasn't Successful When Following Graham

Buffett made the Forbes list for the first time in 1983. This was a year before he gave The Superinvestors of Graham-and-Doddsville speech, and three years before he wrote the above preface.

His personal net worth at the time was $620 Million, which in 1983 is the equivalent of about $2.5 Billion today; when adjusted for inflation.

Of course, thirty more years of investing have taken Buffett's net worth much further than inflation alone would have. But that's the whole point of investing in the first place, to stay well ahead of inflation.

Graham's framework got a man who was 30 years younger, to the equivalent of $2.5 Billion today. If you were in your early Fifties today and worth $2.5 Billion, would you call the framework you have been following unreliable?

Or would you too be giving a speech called The Superinvestors of Graham-and-Doddsville?

Why The Skepticism?

During Graham's time, the argument was often made that his ideas could not possibly be successful. Now when they have proven so successful, the argument is made that those who did succeeded didn't actually follow them. This is in spite of the repeated assertions to the contrary, by Graham's own followers.

The truth is that Graham's principles go against the cognitive biases of the average investor. The stock market seems like an incredibly complex place, and so one assumes the secret to investing success must also be equally complex. That something as conceptually straightforward (though statistically challenging) as Value Investing could be the answer seems downright impossible.

But the fact is that Buffett himself has consistently credited Graham for his investment acumen, as described above. If anything, Munger seems to have steered Buffett away from cigar butt stocks, towards following Graham's Value Investing principles in their entirety.

Irving Kahn, one of Graham's oldest students, passed away a few months ago.

To quote a line from the Bloomberg article on Kahn's passing:

"In 2012, at 106, Kahn told Bloomberg Businessweek that Graham's principles, though relevant as ever, were increasingly being drowned out by noise."

"You stick to value, to Benjamin Graham, the man who wrote the bible for the market. It’s a mistake to believe you can do more."

Buying a wonderful company at a fair price is just as much a part of Value Investing, as is buying a fair company at a wonderful price.

Benjamin Graham did recommend paying more for quality and growth. His only prerequisite was that there be the Margin of Safety between Price and Value.

While the popular interpretation of the Margin of Safety today is to buy stocks with low P/E and P/B ratios, a true Graham Margin of Safety is both qualitative and quantitative.

Here's a note on Value and Growth from Warren Buffett's 1992 letter to shareholders:

"Most analysts feel they must choose between two approaches customarily thought to be in opposition: "value" and "growth... In our opinion, the two approaches are joined at the hip: Growth is always a component in the calculation of value, constituting a variable whose importance can range from negligible to enormous and whose impact can be negative as well as positive."

Growth Investing is not an alternative to Value Investing.

Growth and Quality, as taught by Graham, have always been a part of the Value equation.

Size - The Anchor of Performance

In The Superinvestors of Graham-and-Doddsville, Buffett explains how the size of his portfolio is also his biggest handicap. The closer one's portfolio comes in size to the market itself, the harder it becomes to beat the market average (by definition).

Buffett also cannot buy and sell stocks in the open market at the same average prices the ordinary investor can. His trades alone would drive stock prices beyond Graham's limits.

Thus, most of Buffett's investments today are what Graham defined as Special Situations. Buffett simply has no other choice. But the size of his portfolio gives him advantages specific to institutional investors - controlling interests, preferential treatment, fewer protective regulations, lower commissions etc.

But the rest of us can actually do better percentages by simply following the more automated forms of Value Investing - Defensive, Enterprising and NCAV stocks, and Index Funds. We just need to have the emotional discipline (as Buffett says) to stay the course.

In fact, Buffett himself recommends an S&P500 Index Fund as a good alternative investment in his 2013 letter to shareholders. GrahamValue's own 2+ year old article - How To Build A Complete Benjamin Graham Portfolio - had recommended a Vanguard S&P500 index fund as a good application of Graham's first strategy for investors, and covers Special Situations as well.

To Conclude

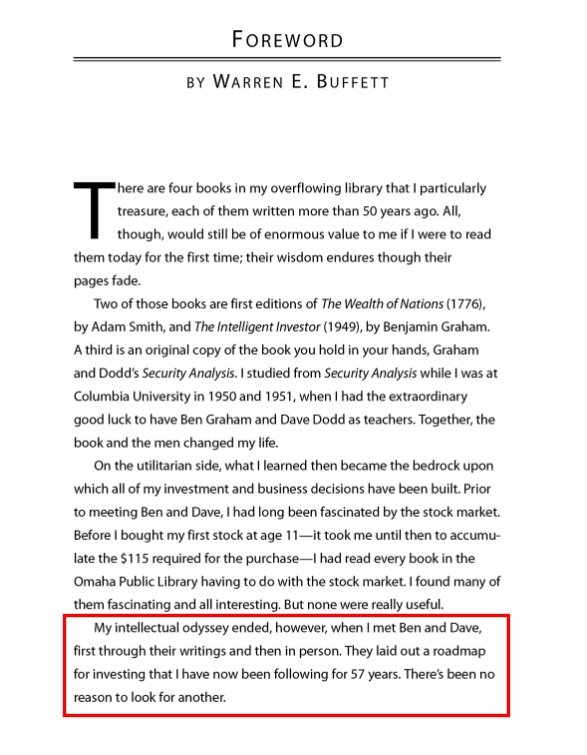

In his 2008 foreword to the sixth edition of Security Analysis, Buffett wrote:

"My intellectual odyssey ended, however, when I met Ben and Dave, first through their writings and then in person. They laid out a roadmap for investing that I have now been following for 57 years. There’s been no reason to look for another."

Most misconceptions about Value Investing arise from incomplete or incorrect information about Graham's principles. If one were to study them thoroughly, there's almost no discrepancy between what Graham taught and what his students follow (as Buffett himself has said many times over).

For example, Graham never specified any rules for selling in his Index Stocks strategy. They were to be held for life. The "sell at 50-100% gains or after 2-3 years" rule is attributed to one of Graham's interviews, and is not verifiable in print. It's not mentioned in any of Graham's books, which have multiple references to Graham's actual recommendations on selling.

Then there's also the highly misunderstood "growth" formula that is wrongly attributed to Graham.

Given below is the conclusion from the study "The Evolution of the Idea of Value Investing: From Benjamin Graham to Warren Buffett" by Robert F. Bierig, Duke University:

"A naive observer of Buffett today would find it difficult to see the Ben Graham influence in many of his activities. However, that influence remains at the core of Buffett’s investment model. Buffett continues to think about stocks as fractional ownership interests in underlying businesses, he continues to operate under the assumption that there is a distinction between price and value, and he continues to search for the largest discrepancy between those two items. In other words, he continues to be a value investor."

Is Warren Buffett a bargain hunter? He once was, a long time ago. But not anymore.

Is Warren Buffett a Value Investor in the way Benjamin Graham truly intended? Yes. Absolutely!

Buffett Videos

On Munger and Graham

Buffett says at the Berkshire Hathaway 1997 Annual Shareholders Meeting that while he owes Charlie Munger a lot, it doesn't compare with what he owes Graham.

Offered To Work For Free

Buffett talks a little more in detail about his working and personal relationship with Graham, naming his son after Graham, and the time he offered to work for Graham for free.

Facebook Likes and Comments

Irving Kahn, Bloomberg Business: How to Play the Market (2012)

Warren Buffett, Preface (1986): The Intelligent Investor by Benjamin Graham

Warren Buffett, Foreword (2008): Security Analysis by Benjamin Graham

Submitted by GrahamValue. Created on Thursday 4th June 2015. Updated on Tuesday 1st August 2023.